When additional funds are required, two frequently used alternatives are personal loans and credit cards. In both ways, you are granted a certain amount of credit; however, they function differently. Selecting the most appropriate can not only cut money and ease your financial worries. In 2025, let’s examine the differences between personal loans and credit cards.

What is a Personal Loan?

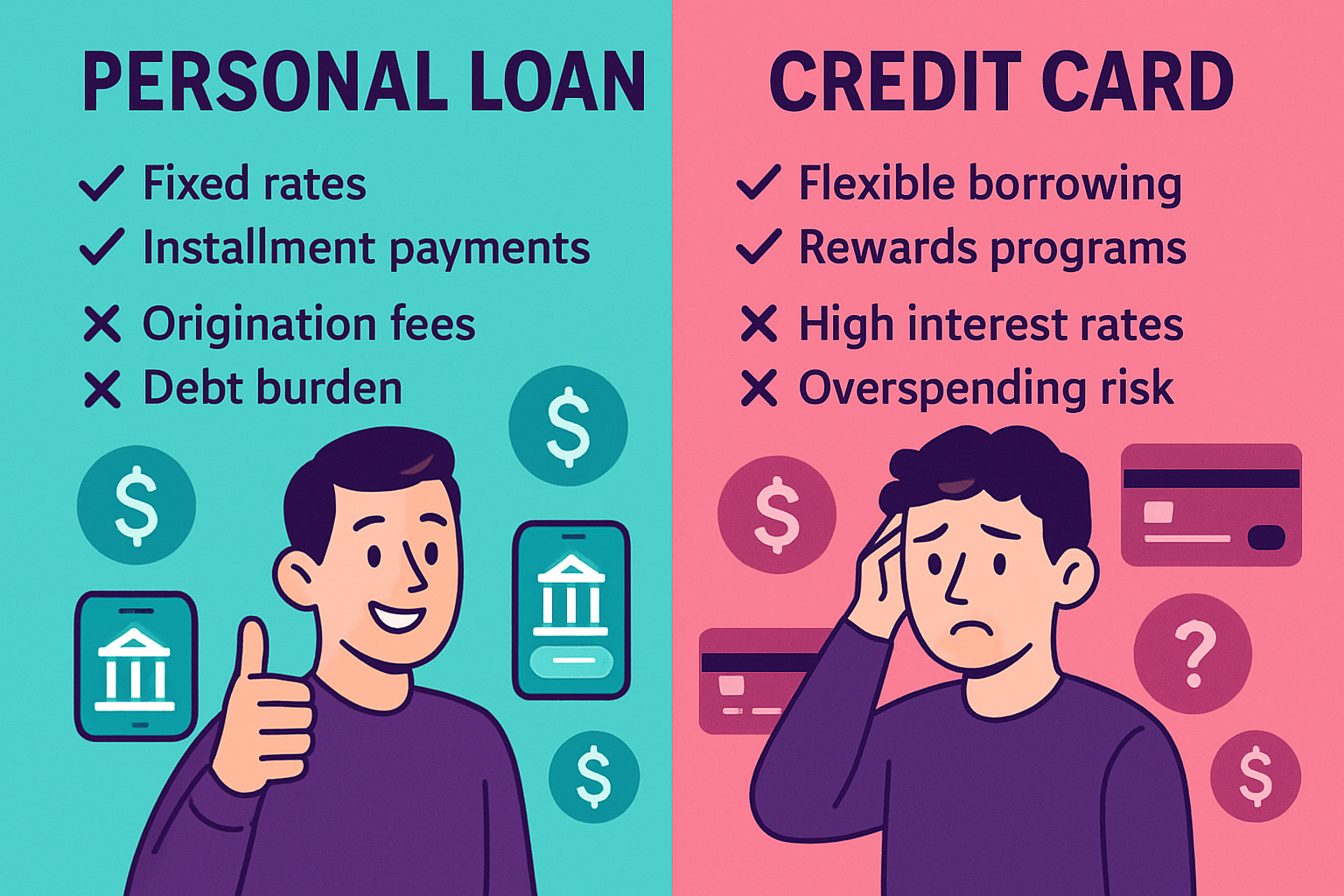

- A personal loan is a single amount of money that you can borrow from a bank, a credit union, or an online lender.

- Fixed interest rate – generally ranging from 6% to 20% APR, depending on the borrower’s credit score.

- Fixed repayment term – usually from 1 to 7 years.

- Monthly payments are set – you know the amount and it is easy to make your budget.

👉 Most appropriate for: Major expenses such as debt consolidation, home renovation, medical bills, or weddings.

What is a Credit Card?

A credit card allows you to have a revolving line of credit which implies that you can keep borrowing as well as repaying regularly.

- Variable interest rates – usually 20%–30% APR.

- Minimum monthly payments – you are allowed to make a payment of your choice, but it usually leads to long-term debt.

- Rewards & perks – cashback, travel miles, or discounts.

👉 Best for: Everyday purchases and short-term borrowing (if you pay off the balance monthly).

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Interest Rates | 6%–20% APR (fixed) | 20%–30% APR (variable) |

| Repayment | Fixed term (1–7 years) | Flexible, revolving credit |

| Loan Amount | £1,000–£50,000 (UK) / $1,000–$100,000 (USA) | £500–£10,000 / $500–$20,000 typical |

| Best Use Case | Debt consolidation, big expenses | Everyday spending, short-term needs |

| Risk of Debt | Lower (structured payments) | Higher (minimum payments trap) |

Which One Should You Choose?

Choose a personal loan if:

- You need a big amount of money at once.

- You desire a lower interest rate

- You like having a fixed monthly payment.

Choose a credit card if:

- You only need to borrow for a short time.

- You want to get some rewards or cashback.

- You are able to pay your balance off in full every month.